Student Loans in USA: 5 vital facts for funding education.

Funding higher education is one of the most significant financial commitments an individual can make, and understanding **Student Loans in USA** is the cornerstone of this process. With tuition costs rising annually, the vast majority of students—both domestic and international—rely on some form of lending to bridge the gap between savings and university fees. However, the system is complex, bifurcated into federal and private sectors, each with distinct rules regarding interest, repayment, and eligibility. This guide breaks down the 5 vital facts you must understand about **Student Loans in USA** to avoid long-term debt traps and finance your degree smartly in 2026.

Table of Contents

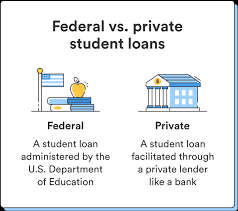

1. Federal vs. Private: The Core Divide in Student Loans in USA

The most critical distinction when researching **Student Loans in USA** is the source of the funds. Loans are categorized as either Federal (funded by the government) or Private (funded by banks, credit unions, or online lenders).

Fact #1: Federal Loans Offer Superior Protections

Federal loans are generally the first choice for eligible students (US citizens and permanent residents). They offer benefits that private loans rarely match, such as income-driven repayment plans and fixed interest rates that are not dependent on credit history. Accessing these requires filling out the FAFSA (Free Application for Federal Student Aid). In contrast, private loans act like standard bank loans; they require a credit check, often need a co-signer, and have stricter repayment terms. Understanding this hierarchy is essential for managing Student Loans in USA.

2. Interest Rates: Understanding the Cost of Student Loans in USA

Interest rates determine the actual cost of your degree over time. The landscape for 2026 shows trends toward stabilization, but rates remain a significant factor.

Fact #2: Fixed vs. Variable Rates

Federal loans always carry **fixed interest rates**, meaning the rate remains the same for the life of the loan. This provides predictability for budgeting. Private **Student Loans in USA**, however, often offer a choice between fixed and **variable rates**. While a variable rate might start lower, it can fluctuate with the market index (like SOFR), potentially causing monthly payments to skyrocket unexpectedly. For most students, locking in a fixed rate is the safer strategy to avoid future financial shock.

Federal vs. Private Loan Comparison (2026 Estimates)

| Feature | Federal Loans | Private Loans |

|---|---|---|

| Interest Type | Fixed Only | Fixed or Variable |

| Credit Check | Not Required (mostly) | Required (Strict) |

| Forgiveness | Possible (PSLF) | Rare / Non-existent |

3. Repayment Plans and Forgiveness: Managing Student Loans in USA

The flexibility of repayment is where the true value of the US system lies, provided you choose the right path.

Fact #3: Income-Driven Repayment (IDR) is a Safety Net

For federal loans, IDR plans cap your monthly payments at a percentage of your discretionary income. If your earnings are low after graduation, your payment could legally be $0. This ensures that Student Loans in USA do not cause bankruptcy. Furthermore, after 20-25 years of payments (or 10 years for public servants under PSLF), the remaining balance may be forgiven. Private lenders generally do not offer these protections, making default a higher risk.

4. International Student Options: Navigating Student Loans in USA

For non-citizens, the path to securing funding is much narrower, as they are typically ineligible for federal aid.

Fact #4: The Necessity of a US Co-Signer

Most international students seeking Student Loans in USA must apply through privatelenders. The vast majority of these lenders require a co-signer who is a US citizen or permanent resident with good credit. This co-signer agrees to take responsibility for the loan if the student cannot pay. Finding a co-signer is often the biggest hurdle for international applicants.

Fact #5: Lenders Without Co-Signers Exist but Cost More

There is a niche market of lenders (such as MPOWER or Prodigy Finance) that offer loans to international students without a co-signer. However, these Student Loans in USA often come with significantly higher interest rates to offset the lender’s risk. Students should carefully calculate the long-term cost before signing.

Financial Planning is Crucial

Because loans must be repaid with interest, minimizing the amount you borrow is vital. We recommend reviewing our guide on Latest US Study Updates to understand the total cost of attendance and financial proof requirements before taking out a loan.

For the most accurate and official information regarding federal aid eligibility and loan types, always refer to StudentAid.gov , the definitive source for US government funding.

Successfully utilizing Student Loans in USA requires a strategic approach. By prioritizing federal options, locking in fixed rates, and understanding the repayment landscape, you can invest in your education without compromising your future financial stability. Whether you are a domestic or international student, knowledge is your most valuable asset in managing educational debt.